Equity Research Deep Dive: Applied Optoelectronics, Inc. (AAOI) – Navigating the 800G Inflection Point and the Multi-Year AI Infrastructure Cycle

By Alex - February 28, 2026

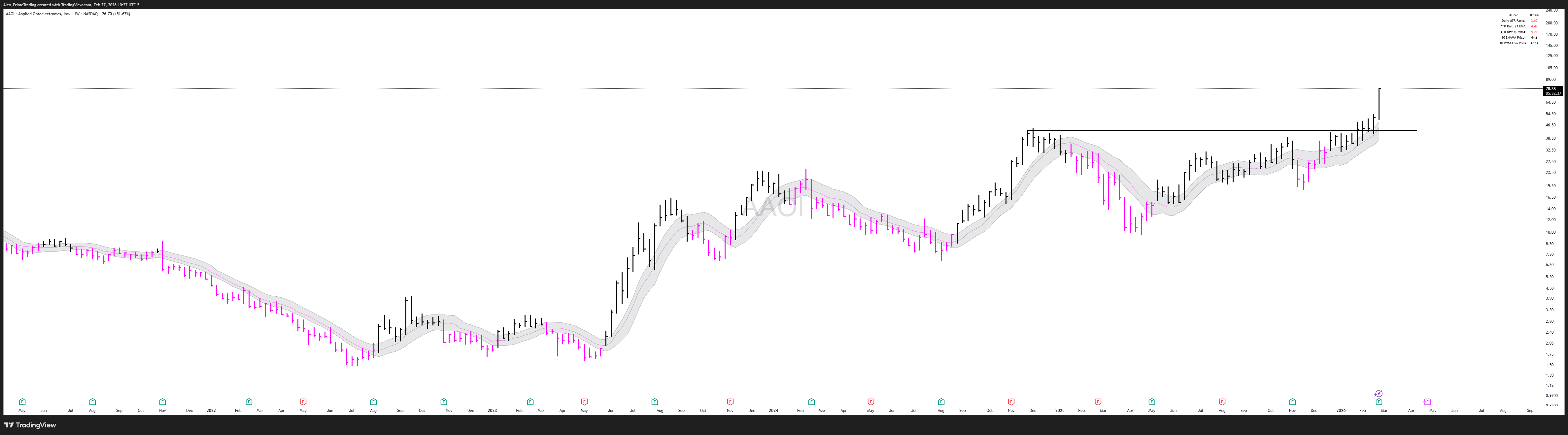

The fourth-quarter 2025 earnings results for Applied Optoelectronics, Inc. (AAOI), released on February 26, 2026, signify a fundamental shift in the company’s operational trajectory and market valuation. Long viewed as a cyclical provider of optical components for the cable television (CATV) and fiber-to-the-home (FTTH) markets, the company has successfully repositioned itself as a vertically integrated cornerstone of the high-speed data center ecosystem required for generative artificial intelligence (AI). The reporting period was defined by a massive upward revision to full-year 2026 revenue guidance, a significant bottom-line beat despite ongoing net losses, and a complex narrative regarding the transition from 400G to 800G and 1.6T transceiver architectures. While the company faces the traditional challenges of a high-growth semiconductor firm—including extreme capital intensity, customer concentration, and the technical hurdles of firmware optimization—the underlying data suggests a “coiled spring” effect where massive capacity investments are finally aligning with an insatiable market demand for optical interconnects.

Structural Foundation: Business Model and Vertical Integration

Applied Optoelectronics operates as a leading, vertically integrated provider of fiber-optic networking products, serving three primary end-markets: internet data centers, cable television, and fiber-to-the-home. To understand the current earnings momentum, one must first analyze the company’s unique manufacturing philosophy. Unlike competitors who often operate as “fab-lite” or outsource the fabrication of core laser components to foundries, Applied Optoelectronics maintains total control over the production cycle, beginning with the fundamental building blocks of lasers and laser components.

The company designs and manufactures a wide range of optical communication products across varying levels of integration, from discrete components and subassemblies to complete modules and turn-key equipment. This vertical integration strategy is not merely a cost-saving measure; it is a mechanism for rapid product development and fast response times to customer requests, which are critical in a market defined by 18-month product cycles. By manufacturing the majority of the laser chips and optical components used in its products, the company provides a simplified supply chain for network equipment manufacturers who seek to lower costs by sourcing integrated modules rather than discrete parts.

The geographic footprint of these operations is strategically distributed across the United States, China, and Taiwan. Research and development facilities are concentrated in Atlanta, Georgia, while engineering and manufacturing are conducted at the corporate headquarters in Sugar Land, Texas, as well as in Taipei and Ningbo. This global distribution allows the company to balance production costs while protecting intellectual property and maintaining close coordination with a global customer base. However, as geopolitical tensions and supply chain sovereignty become paramount, the company’s focus has shifted heavily toward its Texas and Taiwan facilities, particularly for its most advanced 800G and 1.6T transceiver lines.

The Technological Moat: Molecular Beam Epitaxy (MBE)

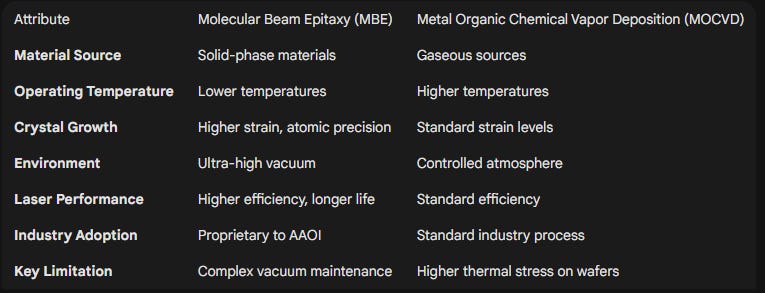

The primary technical differentiator—and the core of the company’s competitive advantage—is its use of Molecular Beam Epitaxy (MBE) for semiconductor laser manufacturing. While the vast majority of the communication optics industry utilizes Metal Organic Chemical Vapor Deposition (MOCVD), Applied Optoelectronics has pioneered a proprietary MBE fabrication process that it believes is unique in the industry.

The MBE process involves growing wafers using solid-phase materials within complex, custom-manufactured ultra-high vacuum equipment. This technique operates at significantly lower temperatures than MOCVD, which allows for the growth of more highly strained crystals and provides atomic-level control over the crystal lattice. The resulting lasers demonstrate improved efficiency, lower threshold currents, and enhanced operating lives. Crucially for the CATV and FTTH markets, these lasers are highly tolerant of fluctuations in temperature and humidity, making them ideal for the harsh outdoor environments where networking equipment is frequently installed.

However, this technological moat is a double-edged sword. The unique nature of the MBE process means that if the specialized facility in Sugar Land were damaged, competitors using MOCVD could not easily replicate the company’s technology, creating a concentration risk that management must mitigate through its Taiwan expansion. Additionally, the MBE process has specific technical limitations, such as the inability to use certain dopant materials like Iron and difficulties with certain types of regrowth. Despite these challenges, the company has developed proprietary circuitry to correct deficiencies like “chirp” and wavelength drift, enabling high-performance signal transmission over long distances that remains a hallmark of its product portfolio.

Table 1: Technical Comparison – MBE vs. MOCVD

Market Positioning and Strategic Grouping

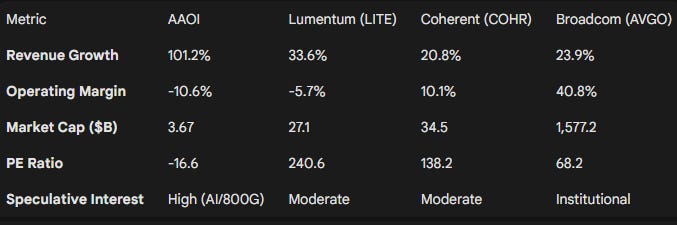

Applied Optoelectronics occupies a distinct niche in the “Zacks Electronics - Semiconductors” industry and the broader optical communications sector. It is frequently compared to larger, more established peers such as Coherent (COHR), Lumentum (LITE), Ciena (CIEN), and semiconductor giants like Broadcom (AVGO) and Marvell (MRVL).

Within this group, Applied Optoelectronics is characterized as a “high-growth, high-risk” player. As of early 2026, its market capitalization of approximately $3.67 billion is significantly smaller than Coherent’s $34.5 billion or Lumentum’s $27.1 billion, yet its trailing twelve-month revenue growth of over 100% dramatically outpaces its larger rivals. This growth is primarily fueled by the company’s ability to capture early market share in the transition from copper to fiber in both data centers and broadband access networks.

The company’s “open system architecture” strategy in the data center market allows its optical connectivity solutions to be used independently of server and switch vendors, which is a major draw for hyperscale operators like Microsoft and Amazon who wish to avoid vendor lock-in. This positioning has allowed the company to become a named collaborator on high-performance platforms, such as the NVIDIA Spectrum-X platform, which utilizes co-packaged optics (CPO) and silicon photonics to support multi-trillion-parameter AI factories.

Table 2: Peer Performance Comparison (LTM Data)

The data indicates that while Applied Optoelectronics lags in profitability, its top-line trajectory is a direct result of its specialized focus on the most bandwidth-intensive segments of the market. The -10.6% operating margin reflects the massive capital investments the company is making into 800G and 1.6T production capacity, a strategy that analysts suggest may lead to “pain now for gain later”.

Analysis of Fourth Quarter and Full Year 2025 Results

The Q4 2025 earnings report delivered a multi-layered surprise to the market. The company achieved record revenue while significantly narrowing its losses, signaling that the massive investments made throughout 2024 and 2025 are beginning to yield results.

Top-Line and Bottom-Line Performance

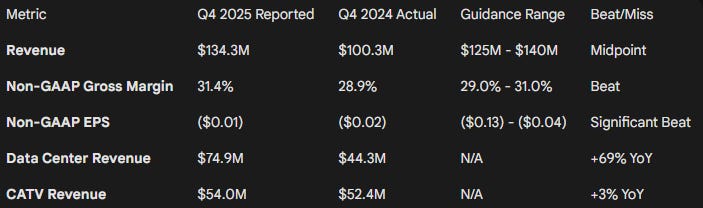

For the quarter ended December 31, 2025, Applied Optoelectronics reported revenue of $134.3 million, a 34% increase from $100.3 million in the prior-year period. This figure was in line with management’s guidance of $125 million to $140 million and essentially met the Zacks Consensus Estimate. More impressively, the non-GAAP net loss narrowed to just $600,000, or $0.01 per share, which was a massive beat compared to the analyst expectation of a $0.11 to $0.13 per share loss.

This beat on the bottom line was driven by a non-GAAP gross margin of 31.4%, which exceeded the top end of the 29% to 31% guidance range and improved from 28.9% year-over-year. The margin expansion is particularly notable because it occurred during a period of heavy capital expenditure and while the company was still absorbing the costs of ramping up new facilities.

For the full year 2025, total revenue increased 83% to a record $456 million. This growth was driven by a diverse set of catalysts: data center revenue rose 32% to $196 million, while CATV revenue nearly tripled to $245 million over the same period.

Table 3: Summary of Q4 2025 Financial Results

Segment Performance and Customer Concentration

The revenue mix for the fourth quarter reflected the company’s deepening penetration into the AI data center market. Data center products accounted for 56% of total revenue, followed by CATV at 40%, with telecom and FTTH making up the remaining 4%.

Data Center Segment: Revenue surged 69% year-over-year and 70% sequentially from Q3. Within this segment, 400G sales increased by 141% year-over-year, while 100G sales rose 54%. This segment’s strength was the primary driver of the margin expansion, as the higher-speed transceivers carry significantly better pricing power than legacy products.

CATV Segment: Revenue of $54 million was down 24% from a record third quarter. Management noted that this sequential decline was expected and was tied to the timing of deployments for 1.8 GHz amplifiers to its largest customer, Charter.

Customer Concentration: A persistent risk factor for the company remains its reliance on a narrow base of customers. The top 10 customers represented 96% of total revenue in Q4. Specifically, one CATV customer accounted for 39% of total revenue, while two data center customers accounted for 31% and 21%, respectively. The data center customers are widely understood to be Microsoft and Amazon, highlighting the company’s success in qualifying for the world’s largest AI infrastructure buildouts.

Transcript Insights: The 800G “Firmware Delay” and the Q2 Ramp

The earnings call provided critical context for the quarter’s results, particularly regarding the performance of the 800G product line. While the company achieved its fourth major 800G volume order from a hyperscale customer during the quarter, revenue from these products actually came in below expectations.

The March Qualification Catalyst

Management explained that 800G revenue was between $4 million and $8 million lower than anticipated due to ongoing “firmware optimizations” required by a key customer, likely Amazon. These optimizations are part of the final qualification process for the 800G transceivers. Dr. Thompson Lin and Stefan Murry confirmed that these firmware customizations are expected to be completed and qualified by mid-March 2026.

This delay, while impacting Q4 numbers, has created a “spring-loaded” revenue potential for the second quarter of 2026. Management explicitly stated that they expect a “major production ramp” to begin in Q2, with 800G revenue potentially exceeding $25 million in that quarter alone. More importantly, management confirmed that current demand for 800G and 1.6T products outpaces their total production capacity through mid-2027, indicating that the company’s growth is “limited by our production capacity and supply chain, not market demand”.

Operational Scaling and Capacity Targets

A significant portion of the call was dedicated to the massive expansion of manufacturing facilities in Texas and Taiwan.

End-of-2025 Status: The company reached a production capacity of approximately 90,000 800G units per month by year-end, with about 31% of that capacity based in the U.S..

2026 Targets: The company is aggressively scaling to reach more than 500,000 combined 800G and 1.6T units per month by the end of 2026. Approximately 25% of this total capacity is expected to come from the Texas facility.

Revenue Potential: Rosenblatt analysis suggests that by the second half of 2027, the company could be generating $378 million in monthly transceiver revenue, divided between $90 million for 100G/400G, $217 million for 800G, and $71 million for 1.6T.

This transition from 400G to 800G and eventually 1.6T is the fundamental driver of the company’s long-term margin expansion thesis. Management expects gross margins to improve from the current 31% level to above 35% by year-end 2026 and above 40% by the end of 2027, as the mix shifts toward these more complex, higher-margin products.

Strategic Expansion: The Sugar Land, Texas Hub

The decision to expand domestic manufacturing is perhaps the most strategic move in the company’s recent history. On February 13, 2026, the company broke ground on a new 210,000-square-foot manufacturing facility in Sugar Land, Texas. This project, supported by a $2 million incentive package from the city, is expected to create 500 jobs and marks the single largest production increase in the company’s history.

Onshoring as a Competitive Edge

In a market increasingly sensitive to supply chain sovereignty and geopolitical risks, having the largest U.S.-based manufacturing capacity for AI-focused transceivers is a significant competitive advantage. Management has been vocal about its efforts to achieve “near-zero” China content in its advanced components, noting that less than 10% of the value in its 800G/1.6T modules currently originates from China.

This onshoring strategy is enabled by the company’s proprietary automation technology. Over the past decade, Applied Optoelectronics has invested heavily in in-house automation, spanning mechanical design, machine vision, and AI-assisted inspection. This automation allows the company to rapidly replicate its production lines in Texas, ensuring that U.S.-based manufacturing remains globally competitive with the lower labor costs of Asia. The new facility is designed to use the same manufacturing equipment for both 800G and 1.6T products, providing the flexibility to shift production based on maturing demand.

Financial Strategy: The $250 Million ATM Agreement

To fund this massive expansion, Applied Optoelectronics announced a $250 million at-the-market (ATM) equity distribution agreement with Raymond James & Associates and Needham & Company on February 26, 2026. This agreement allows the company to issue and sell shares of common stock from time to time at prevailing market prices.

Purpose and Dilution

The proceeds from the offering are intended for general corporate purposes, which include debt repayment, working capital, and crucially, capital expenditures for the new manufacturing facilities. While the flexibility of an ATM program is beneficial for a high-growth company, it does represent a risk of dilution for existing shareholders. As of February 25, 2026, the company had approximately 75.2 million shares outstanding. An illustrative sale of 4.3 million shares at a price of $58.12 would raise the full $250 million but would result in dilution to new and existing investors.

The company’s financial position is currently robust enough to support its short-term obligations, with a current ratio of 2.31. However, the net loss of $38.2 million for the full year 2025 and an accumulated deficit of $493.1 million highlight the ongoing financial vulnerability that necessitates this external capital. The aggressive CapEx schedule—which reached $209 million in 2025 and is expected to be even higher in 2026—means that the company’s path to positive free cash flow remains dependent on the successful execution of the 800G ramp.

Macro Trends: Copper vs. Fiber and the AI Bottleneck

The fundamental thesis for Applied Optoelectronics is built on the physical limitations of traditional networking infrastructure. As data centers expand to support generative AI workloads, traditional copper interconnects are hitting a “copper wall” where they are limited by distance, data rate, and thermal constraints.

The Optical Interconnect Revolution

Optical interconnects have become the only viable solution for the high-density, low-latency communication required by clusters of hundreds of thousands of GPUs. This is why hyperscalers are aggressively upgrading their optical infrastructure to 800G and 1.6T. TrendForce projects that global shipments of 800G-and-above transceivers will leap from 24 million units in 2025 to nearly 63 million in 2026—a 2.6x jump in a single year.

Applied Optoelectronics is positioning itself at every layer of this transition:

Laser Sources: Providing the high-power lasers that serve as the foundation of the optical signal.

Transceiver Modules: Manufacturing the pluggable modules (DR8, OSFP) that convert electrical signals to optical and back again.

Co-Packaged Optics (CPO): Developing the next-generation architecture where optical engines are integrated directly next to the switch ASIC, reducing power consumption by 3.5x and increasing reliability by 10x.

NVIDIA’s Rubin platform, expected to ramp in late 2026, is designed from the ground up to integrate silicon photonics networking. Applied Optoelectronics’ announcement of a new 400mW narrow-linewidth pump laser is a direct play for this emerging CPO space, as these lasers are critical for the power-efficient switching required by next-generation AI factories.

Broadband and CATV: The Secondary Growth Engine

While the data center segment captures the headlines, the company’s CATV business provides a significant, higher-margin secondary engine for growth. The industry is currently in the midst of a transition to DOCSIS 4.0, which requires cable operators to upgrade their hybrid fiber-coaxial (HFC) networks to support symmetrical multi-gigabit speeds.

1.8 GHz Amplifiers and QuantumLink

The company has successfully certified its 1.8 GHz amplifiers and QuantumLink remote management software with Charter. These products are essential for operators who are upgrading their legacy infrastructure to meet the bandwidth demands of modern residential and business users. Management believes that the 2026 target of $300 million in CATV revenue is achievable, driven by the rollout of these new amplifiers and node equipment.

The customization of these CATV products creates high switching costs and longer product lifecycles, which helps to stabilize the company’s overall revenue stream. By the end of 2025, the company had 17 CATV customers globally, and it is gaining market share as equipment vendors increasingly outsource both the design and manufacture of headend and node equipment to vertically integrated providers like Applied Optoelectronics.

Analyst Ratings and Valuation Scenarios

The investment community is currently divided into two camps regarding Applied Optoelectronics. One camp views the company as an undervalued AI play with massive revenue potential, while the other remains cautious about its valuation and execution risks.

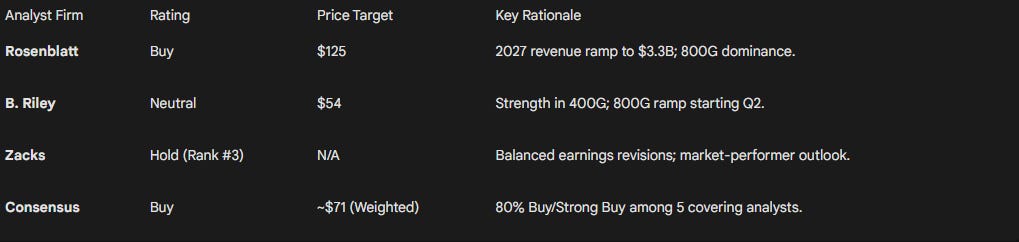

The Bull Case: Rosenblatt’s $125 Target

The most bullish outlook comes from Rosenblatt, which raised its price target to $125 from $75 following the Q4 results. This target is based on 20 times the firm’s calendar year 2027 earnings per share forecast of $6.25. Rosenblatt expects the company to achieve $1.02 billion in revenue and $1.18 in EPS in 2026, followed by a massive surge to $3.3 billion in revenue and $6.25 in EPS in 2027.

The Neutral Perspective: B. Riley’s Upgrade

B. Riley recently upgraded the stock from “Sell” to “Neutral” and raised its price target to $54 from $15. This upgrade was driven by the continued strength in 400G products and the expected growth from 800G starting in the second quarter. While B. Riley acknowledges the strong momentum, they remain watchful of the company’s ability to scale 800G production profitably.

The Bear Case: Valuation and Concentration Risks

Bearish analysts highlight that the stock trades at 84x forward earnings and that its massive gains—surging 123% over the past year—may have already priced in the 800G growth story. Concerns persist about the company’s reliance on two customers for 88% of its revenue and the potential for margin pressure if competitors like Jabil (JBL), which recently acquired Intel’s silicon photonics unit, successfully scale their own 800G solutions.

Table 4: Analyst Price Target Summary

Operational Risks and Contradictions

While management provides an optimistic outlook, some industry reports present a more cautious or even skeptical view of the company’s readiness to dominate the 800G market. For instance, some investigative reports have questioned whether the company’s Taiwan expansion is as advanced as claimed, suggesting that construction at the new site may be behind schedule.

Management’s response to such concerns has been to focus on actual order intake and qualification milestones. The announcement of the fourth 800G volume order and the breaking of ground in Sugar Land serve as tangible proof points against claims of a lack of production capability. Furthermore, the qualification of 400G products—which surged 141% in Q4—demonstrates the company’s ability to successfully scale high-speed optical transceivers for hyperscale customers.

Another risk is the potential for supply chain constraints, particularly in laser components. While the company is vertically integrated, it still relies on third-party suppliers for certain sub-components and specialized materials. Any disruption in these supplies could hinder the aggressive manufacturing ramp scheduled for late 2026.

Conclusion: A Multi-Year Growth Narrative

Applied Optoelectronics has emerged from 2025 as a significantly more powerful and strategically aligned company than it was at the beginning of the year. The fourth-quarter results confirmed that the “AI optical boom” is not merely a theoretical catalyst but a tangible driver of record revenues and expanding gross margins.

The narrative for 2026 is clearly defined: it is the year of the 800G ramp. By overcoming the final firmware optimizations in March, the company is poised to unleash its expanded manufacturing capacity in Texas and Taiwan to meet a demand environment that currently exceeds its production capabilities. The guidance of over $1 billion in 2026 revenue marks a transformative milestone that, if achieved, will firmly establish the company as a top-tier player in the global semiconductor networking sector.

Investors must weigh the high valuation and capital-intensive nature of this growth against the company’s unique technological moat (MBE) and its strategic domestic manufacturing footprint. While risks regarding customer concentration and technical execution remain, the fundamental transition from copper to fiber in AI data centers provides a powerful multi-year tailwind that Applied Optoelectronics is uniquely positioned to capture. The next several quarters will be critical as the market monitors the 800G ramp-up, the first shipments of 1.6T transceivers, and the company’s progress toward achieving sustained, high-margin profitability.

PrimeTrading is an equity trading community for learning & trading alongside experienced traders. It’s like sneaking into a trader’s POD, where you can see us execute & discuss...but in ours, you can also interact and ask questions.

I would have killed for such an opportunity when I started trading! 🔥

Education & mentoring from Alex & experienced traders. (10 Experienced Traders team)

See how I execute intraday while I share all my trades with explanations live.

Alex’s daily market commentary, Portfolio updates, trade explanations, and daily FocusList.

Share & Discuss potential trade ideas with an amazing, like-minded community.

Talk Sectors, Macro Economy, Cryptocurrencies & much more!

Talk about mental game & psychology to evolve as a trader!

Live trading and Q&A sessions every morning.

Trade & learn with us, from Novice to Expert!

Best,

Alex 🛡️✌️