The $5 Trillion Pivot: Inside Tesla’s $TSLA Master Plan to Abandon the Assembly Line and Build the Workforce

By Alex - February 28, 2026

If you are still valuing Tesla (TSLA) based on how many Model Ys they delivered last quarter, you are playing a game that ended in 2024.

Following their explosive Q4 2025 earnings call and a flurry of February announcements, the reality of the situation is no longer a secret: Tesla is no longer a car company. They are a Physical AI and Robotics company that happens to fund its R&D through a legacy automotive business.

This isn’t just hyperbole or Elon Musk’s typical “future casting.” The capital expenditure (CapEx) proves it. The factory floor proves it. In Q2 of this year (2026), Tesla will officially kill off the legendary Model S and Model X to convert that massive footprint inside the Fremont factory into a dedicated, mass-production hub for the Optimus humanoid robot.

Wall Street is currently experiencing a violent tug-of-war. Traditional auto analysts are panicking over declining EV market share, while AI analysts are trying to model the total addressable market (TAM) of replacing human labor globally.

Here is the most exhaustive, professional-grade deep dive into the state of the Tesla Empire today—from the hidden cash cow of their energy division, to the granular engineering of the Optimus robot, right down to the fundamental and technical levels you need to trade it.

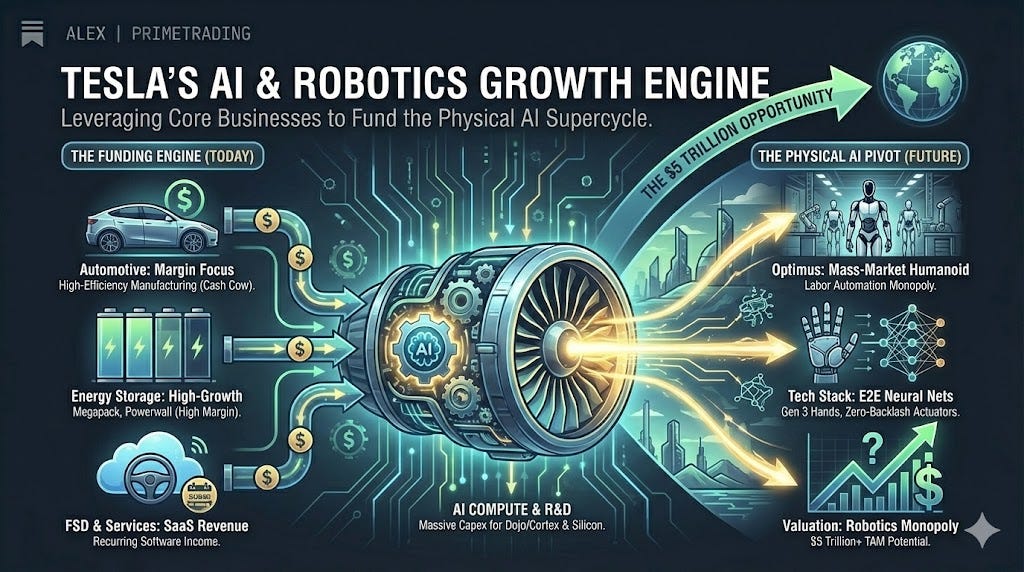

Part 1: The Core Businesses (The Funding Engine)

Before we get to the robots, we have to understand how Tesla is funding this $20+ billion CapEx supercycle.

1. Automotive: Margin Expansion Over Volume

Let’s look at the brutal reality of the EV market: Tesla’s US market share dropped from 49% in 2024 to 46% in 2025. Globally, they have ceded the sheer volume crown to China’s BYD and Geely. Total automotive revenue actually dropped 10% in 2025 to $69.5 billion.

But here is the twist that caught the bears off guard in the Q4 print: Profits went up. By relentlessly focusing on cost of goods sold (COGS) and manufacturing efficiency, Tesla expanded its automotive gross margins (excluding credits) from 15.4% to a staggering 17.7%. They are selling slightly fewer cars, but making significantly more money on each one. The auto division has shifted from a “hyper-growth” story to a “cash-cow” story designed to fund the AI pivot.

2. Energy Storage: The Hidden Giant

If you want to know what saved Tesla’s Q4 earnings, look at the batteries.

The energy generation and storage segment just went parabolic. Tesla deployed a record 46.7 gigawatt-hours in 2025, a massive 48% YoY surge.

The Revenue: Hit $12.8 billion (up 27% YoY).

The Margin: Energy storage is now generating nearly 30% gross margins—almost double the profitability of the car business.

The Catalyst: As the AI boom forces tech giants to build 500MW data centers, grid stability is failing. Utilities are buying Tesla Megapacks by the thousands to store renewable energy and prevent blackouts. Energy is no longer a side project; it is the most robust fundamental pillar of the company today.

3. Services & FSD (Software)

Tesla officially crossed 1.1 million paid Full Self-Driving (FSD) customers globally. However, in early 2026, they executed a major strategic shift: transitioning FSD to a subscription-only model. While this will cause short-term margin compression (no more recognizing $8k upfront cash lumps), it builds a massive, recurring, SaaS-like revenue stream that Wall Street traditionally values at much higher multiples. Furthermore, the “Cybercab” (Robotaxi) has begun unsupervised service testing in Austin, stripping out the safety monitors entirely.

Part 2: The Physical AI Supercycle (The Robotics Deep Dive)

This is the main event. If you want to understand Tesla’s current $250+ P/E ratio, you have to look at Optimus. The humanoid robotics market is projected to be a $5 trillion to $10 trillion industry by 2050, and Tesla is aggressively positioning itself to be the monopoly supplier.

The Strategic Pivot: The Death of S/X

In a move that stunned legacy auto enthusiasts, Tesla announced they are ending production of the Model S and Model X. Why? Because the physical footprint in the Fremont factory is too valuable. Fremont is being retooled right now to become the Optimus mass-production hub, with Elon Musk citing a staggering long-term goal of producing 1 million robots per year from that single facility.

The Tech Stack: An Engineer’s View

Robotics historically failed because they relied on “deterministic code” (hard-coding the exact XYZ coordinates for an arm to move). Tesla threw that out and applied their FSD playbook to a bipedal body.

Pixels-to-Torque Neural Networks: Optimus has no hard-coded pathways. It uses 8 cameras to take in visual data (”pixels”), processes it through an onboard AI chip, and the neural network outputs the exact electrical current (”torque”) to the motors. It learns by watching humans via teleoperation, then generalizes those movements.

Gen 3 Hands (The 50-Actuator Leap): Hands are the hardest problem in robotics. In February 2026, Tesla revealed the Gen 3 hands. Going from 11 Degrees of Freedom (DoF) in Gen 2 to 22 DoF (with a total of 50 actuators across the arm/hand), the bot now possesses tactile sensors that allow for superhuman precision. They can sort fragile battery cells, fold laundry, and handle power tools.

Zero-Backlash Actuators: Tesla designs all of its own rotary and linear actuators (the robot’s muscles). They function similarly to strain-wave gears, allowing for millimeter-precise movements without the “wobble” or “backlash” seen in traditional mechanical joints.

The Deployment Timeline

This isn’t happening in 2030. It is happening right now.

2025 (Completed): Low-volume production (~5,000 units target) for internal R&D.

Q2-Q4 2026: Internal Factory Deployment. Optimus robots will take over repetitive tasks (sorting, parts handling) inside Tesla’s own Gigafactories. This is the crucial “training” phase, during which they gather millions of hours of real-world data.

Late 2026 / 2027: Limited external sales to commercial partners (estimated price: ~$30,000).

2028+: Mass market and consumer availability.

The Ultimate Compute Moat

You cannot train a million robots without unprecedented computing power. Tesla is currently building Cortex 2, a 500-megawatt AI data center dedicated entirely to training Optimus and FSD. They are also moving chip design completely in-house with the upcoming AI5 silicon and the proposed “TerraFab” semiconductor packaging facility to ensure they are never bottlenecked by external suppliers like TSMC.

Part 3: Q4 2025 Earnings Clues & The Smart Money Flow

When you read through the late-January 2026 earnings transcript, a few massive “tells” jump out regarding how institutional money is viewing the stock:

The $20 Billion CapEx Bomb: Tesla guided for over $20 billion in capital expenditures in 2026. This is massive. Traditional auto investors hated this because it eats free cash flow. AI investors loved it because it proves Tesla is buying the compute necessary to win the AGI/Robotics race.

The End of “Unit Volume” Worship: CFO Vaibhav Taneja explicitly stated that software and COGS optimization are now the drivers, not just raw delivery numbers. The era of blindly cheering for “50% vehicle delivery growth YoY” is dead.

The Sovereign Demand: While US consumer EV demand softened, Tesla noted a surge in demand from international markets (Taiwan, Saudi Arabia, Norway).

Part 4: Fundamentals, Valuation & Technicals

How do you value a company that is simultaneously a shrinking auto manufacturer, a booming energy utility, and a speculative robotics monopoly?

The Fundamentals

Current Price: ~$410 - $420

Market Cap: ~$1.3 - $1.4 Trillion

Trailing P/E: ~259x (GAAP EPS was $1.63 in 2025)

Forward P/E: ~100x to 150x (depending on 2026/2027 estimates)

Free Cash Flow: $6.2 Billion in 2025

Cash on Hand: $44.1 Billion

The Valuation Reality: At 259x earnings, Tesla is undeniably, objectively expensive by any traditional metric. You are not buying an auto company at this price. You are paying a massive premium for a call option on Elon Musk successfully commercializing the humanoid robot and the autonomous Cybercab. The energy business provides a profitable floor, but Optimus is what justifies the trillion-dollar valuation.

The Technical Setup (February 2026)

From a charting perspective, TSLA is currently at a critical inflection point following the post-earnings volatility.

The Trend: The stock is down roughly 6% over the last 30 days, pulling back from its 52-week high of $498.83 down into the $410 range.

Moving Averages: TSLA has broken below its 50-day moving average (~$439), which puts it in a short-term bearish/consolidation trend.

The Line in the Sand: The stock is rapidly approaching its rising 200-day moving average at $389. This is the ultimate institutional support level.

The Setup: If TSLA tests the $389–$400 zone and bounces with heavy volume, it creates a pristine “buy the dip” risk/reward setup for swing traders. If it breaks below the 200-day, expect a deeper technical wash-out as impatient momentum money leaves the stock.

Options Flow: Recent unusual options activity shows a heavy slant toward near-term PUTs around the $400 strike, confirming that smart money expects a test of that major support level very soon.

The Bottom Line

The integration of AI into physical robotics has moved past the conceptual R&D stage and is now a measurable, multi-billion-dollar CapEx trend.

If you view Tesla solely through the lens of electric vehicle deliveries, the stock is terrifyingly overvalued and facing stiff global competition. However, if you view Tesla through the lens of its underlying technology stack—a company leveraging a $44 billion cash pile to build the world’s most advanced edge-inference NPUs, zero-backlash actuators, and global AI training centers—it represents the only publicly traded, vertically integrated monopoly play on the Physical AI supercycle.

The next 12 months are highly binary. As Fremont converts to building robots instead of Model S sedans, Tesla must prove that Optimus can generate actual economic value on the factory floor. If they do, the $5 trillion TAM opens up. If they stumble, the 250x P/E ratio will brutally compress.

Trade the technicals, but invest in the bottlenecks.

PrimeTrading is an equity trading community for learning & trading alongside experienced traders. It’s like sneaking into a trader’s POD, where you can see us execute & discuss...but in ours, you can also interact and ask questions.

I would have killed for such an opportunity when I started trading! 🔥

Education & mentoring from Alex & experienced traders. (10 Experienced Traders team)

See how I execute intraday while I share all my trades with explanations live.

Alex’s daily market commentary, Portfolio updates, trade explanations, and daily FocusList.

Share & Discuss potential trade ideas with an amazing, like-minded community.

Talk Sectors, Macro Economy, Cryptocurrencies & much more!

Talk about mental game & psychology to evolve as a trader!

Live trading and Q&A sessions every morning.

Trade & learn with us, from Novice to Expert!

Best,

Alex 🛡️✌️